Governance - How We Govern

The success of the Bank relies on its proven track record in upholding high standards of corporate governance and the Board is committed to ensuring that the governance structures, policies and processes are sufficiently robust and relevant in a fast changing operating environment. This Report provides an insight into how the Board discharges this key responsibility.

The Board of Directors, which is the highest decision making body of Commercial Bank, takes the view that Corporate Governance and Risk Management are the bedrock on which the entire organisation rests, as it guides the Board and all levels of employees in the conduct of business on a day-to-day basis.

It requires a proactive approach to identify areas for improvement and a questioning of the current status quo to ensure that all elements of our governance framework are fit for purpose, enabling value creation and growth, whilst acknowledging the legitimate rights and responsibilities of key groups of stakeholders and preserving accountability. Further, the Banking sector is perhaps the most regulated industry, in order to maintain the right balance between stakeholder rights and obligations, it will be subject to increased regulations in the near future as developments in global markets are swiftly adopted in the countries we operate in.

Consequently, in setting the governance framework for the Bank, the Board takes in to account the regulatory requirements, voluntary codes, international and market best practices and the need to deliver value to its stakeholders in a clear and transparent manner.

The Corporate Governance Framework of the Bank comprises the following:

- Articles of Association of the Bank

- Board Charter

- Organisational Structure

- Terms of Reference and Charters of Board and Management Committees

- Integrated Risk Management Framework

- Code of Ethics for all employees

- Board approved policies on all major operational aspects

Collectively, they ensure compliance with the following major external steering instruments on governance:

- Companies Act No.7 of 2007 which includes provisions for preserving rights of investors

- Banking Act No.30 of 1988 and amendments thereto which contain provisions for preserving the rights of depositors and rights and responsibilities of regulators

- All Directions for Licensed

Commercial Banks issued by the CBSL and Bangladesh Bank for operations This includes Direction No.11 of 2007 on the subject of Corporate Governance for Licensed Commercial Banks in Sri Lanka - Continuing Listing Rules of the Colombo Stock Exchange (CSE) which also address the rights of investors

- Shop & Office Employees Act of 1954 and amendments thereto addressing the rights and responsibilities of employees

- Inland Revenue Act No.10 of 2006 and amendments thereto and numerous legislative Acts which are applicable as a collecting agent for regulatory bodies

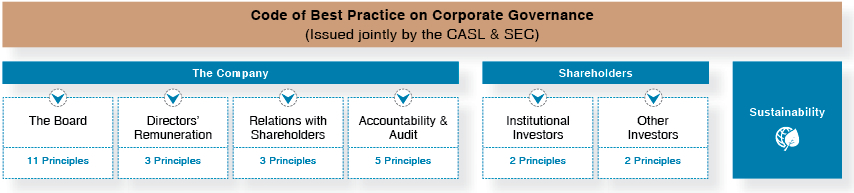

- Code of Best Practice on Corporate Governance issued jointly by the CASL and SEC, which seeks to address how companies govern balancing the rights of key stakeholder groups including the community in which we operate

(Figure 6 below)

This segment of the Report seeks to communicate to our key stakeholders how the Bank is governed. We have used the structure of the Code of Best Practice in Corporate Governance to communicate in a comprehensive but concise manner, the governance structures and processes of the Bank. As Commercial Bank is fully compliant with the requirements of the Banking Act Direction No.11 of 2007, set out on this section the CSE has exempted the Bank from disclosure of compliance with the requirements stipulated in Section 7.10 of the Continuing Listing Requirements on Corporate Governance. Compliance with the Banking Direction No.11 of 2007 on Corporate Governance has been reviewed by the External Auditors, who have provided assurance to the CBSL on same.

Figure - 6

The Board

An Effective Board

(Principle A.1)

The Board of Commercial Bank comprises of 8 eminent professionals in the fields of Banking & Finance, Accounting, Management, Economics and Engineering, whose profiles are given under this report are elected by shareholders at the Annual General Meeting with the exception of the Chief Executive Officer and the Chief Operating Officer who are appointed by the Board and remain as Executive Directors until expiry or termination of such appointments. Casual vacancies are filled by the Board, based on the recommendations of the Board Nomination Committee as provided for in the Articles of Association. They are assisted by the Company Secretary, an Attorney-at-Law, whose profile is given on this report.

The Board provides strategic direction and sets in place a sufficiently robust governance structure and policy framework to facilitate value creation to stakeholders in accordance with applicable laws and regulations.

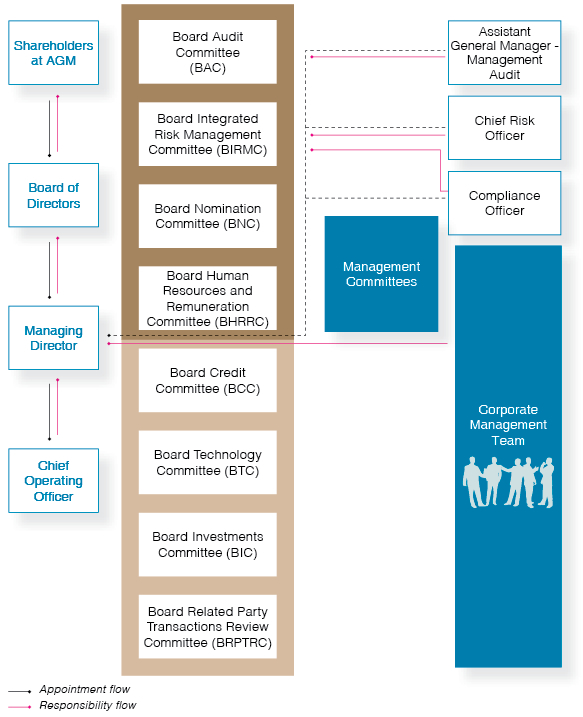

Organisational Structure

A key element of Corporate Governance is an organisational structure that creates a conducive environment for policies to function effectively. Following diagram (Figure 7) provides an overview of the organisational structure of Commercial Bank.

Figure - 7

Board Sub-Committees

There are 8 Board Sub-Committees which comprise of 4 mandatory committees and 4 voluntary committees that have been established considering the business needs of the Bank and best practice in corporate governance as described below (Table 2).

| Board Committee | Areas of Oversight | Composition & Executive Support |

| Mandatory Committees | ||

| Board Audit Committee (BAC) |

for more information. |

|

| Board Integrated Risk Management Committee (BIRMC) |

for more information. |

|

|

Board Nomination Committee (BNC) |

|

|

| Board Human Resources and Remuneration Committee (BHRRC) |

|

|

| Voluntary Committees | ||

| Board Credit Committee (BCC) |

|

|

|

Board Technology Committee (BTC) |

|

|

| Board Investment Committee (BIC) |

|

|

| Board Related Party Transactions Review Committee (BRPTRC) |

|

|

Table - 2

Regular Meetings (Principle A 1.1)

During 2015 the Board held 14 scheduled meetings which included one meeting devoted to strategy whilst 13 meetings were devoted to matters requiring further attention of the Board. The Board Committees also met regularly as summarised below:

Details of the Main Board and Board Sub-Committees as at December 31, 2015

| Name of Committee | Main Board | Board Audit Committee | Board Integrated Risk Management Committee | Board Nomination Committee | Board Human Resources and Remuneration Committee | Board Credit Committee | Board Technology Committee | Board Investment Committee | Board Related Party Transactions Review Committee | |||||||||

| Name of Director | Status | DOA | Status | DOA | Status | DOA | Status | DOA | Status | DOA | Status | DOA | Status | DOA | Status | DOA | Status | DOA |

| Mr. K.G.D.D. Dheerasinghe | C | 20.12.2011 | M** | 19.02.2015 | C | 30.12.2011 | C | 30.12.2011 | C | 30.12.2011 | C | 13.03.2013 | C | 26.12.2014 | ||||

| Mr. M.P. Jayawardena | M | 28.12.2011 | C | 30.12.2011 | M | 29.08.2014 | M | 29.08.2014 | ||||||||||

| Mr. J. Durairatnam | M | 28.04.2012 | I | 28.04.2012 | M | 28.04.2012 | I | 29.08.2014 | I | 29.08.2014 | M | 29.08.2014 | M | 18.06.2012 | M | 13.03.2013 | M | 26.12.2014 |

| Mr. S. Swarnajothi | M | 20.08.2012 | C | 24.08.2012 | M | 24.08.2012 | M | 29.04.2015 | M | 29.04.2015 | M | 26.12.2014 | ||||||

| Mr. H.J. Wilson | M | 03.07.2014 | M | 29.08.2014 | ||||||||||||||

| Mr. S.Renganathan | M | 17.07.2014 | I | 17.07.2014 | I | 29.08.2014 | M | 25.11.2014 | M | 29.08.2014 | M | 29.08.2014 | M | 26.12.2014 | ||||

| Prof. A.K.W. Jayawardane | M | 21.04.2015 | M | 21.04.2015 | M | 29.04.2015 | C | 21.04.2015 | ||||||||||

| Mr. K. Dharmasiri | M | 21.07.2015 | M | 21.07.2015 | M | 21.07.2015 | M | 28.08.2015 | ||||||||||

| Prof. U.P. Liyanage | M* | 14.12.2010 | M* | 01.04.2011 | M* | 25.11.2011 | M* | 30.12.2011 | M* | 30.12.2011 | ||||||||

| Mr. L. Hulugalle | M* | 30.03.2011 | M* | 27.05.2011 | M* | 01.04.2011 | ||||||||||||

| Mr. K.M.M. Siriwardana | M*** | 28.08.2014 | I*** | 28.08.2014 | M*** | 28.08.2014 | ||||||||||||

Table - 3

DOA - Date of Appointment

Status - C - Chairman / M - Member/ I - Participated by Invitation

* Resigned w.e.f. date specified under Item 11.1 of the ‘Annual Report of the Board of Directors'.

** Resigned w.e.f. August 21, 2015

*** Caused to hold office w.e.f. February 23, 2015

Number of Meetings Held and Attendance

| Name of Committee | Main Board | Board Audit Committee | Board Integrated Risk Management Committee | Board Nomination Committee | Board Human Resources and Remuneration Committee | Board Credit Committee | Board Technology Committee | Board Investment Committee | Board Related Party Transactions Review Committee | |||||||||

| Name of Director | Eligible to Attend | Attended | Eligible to Attend | Attended | Eligible to Attend | Attended | Eligible to Attend | Attended | Eligible to Attend | Attended | Eligible to Attend | Attended | Eligible to Attend | Attended | Eligible to Attend | Attended | Eligible to Attend | Attended |

| Mr. K.G.D.D. Dheerasinghe | 14 | 14 | 6 | 6 | 3 | 3 | 5 | 5 | 12 | 12 | 12 | 12 | 1 | 1 | ||||

| Mr. M.P. Jayawardena | 14 | 14 | 4 | 4 | 3 | 3 | 5 | 5 | ||||||||||

| Mr. J. Durairatnam | 14 | 14 | 10 | 10 | 4 | 4 | 3 | 3 | 5 | 5 | 12 | 12 | 3 | 3 | 12 | 12 | 1 | 1 |

| Mr. S. Swarnajothi | 14 | 14 | 10 | 10 | 4 | 4 | 1 | 1 | 5 | 3 | 1 | 1 | ||||||

| Mr. H.J. Wilson | 14 | 13 | 12 | 11 | ||||||||||||||

| Mr. S. Renganathan | 14 | 13 | 10 | 6 | 4 | 3 | 12 | 10 | 3 | 3 | 12 | 10 | 1 | 1 | ||||

| Prof. A.K.W. Jayawardane | 9 | 8 | 7 | 5 | 8 | 7 | 3 | 3 | ||||||||||

| Mr. K. Dharmasiri | 6 | 6 | 3 | 3 | 2 | 2 | 4 | 3 | ||||||||||

| Prof. U.P. Liyanage* | 5 | 1 | 1 | 0 | 2 | 0 | 5 | 0 | ||||||||||

| Mr. L. Hulugalle** | 4 | 2 | 2 | 1 | 1 | 0 | ||||||||||||

| Mr. K.M.M. Siriwardana*** | 3 | 0 | 2 | 1 | ||||||||||||||

Table - 4

* Resigned w.e.f. April 28, 2015

** Resigned w.e.f. March 31, 2015

*** Ceased to hold office w.e.f. February 23, 2015

Notes:

Following members of the Management attended the Board Audit Committee (BAC) meetings by Invitation:

Mr. S. Prabagar (AGM - Management Audit/Secretary of BAC)

Mr. K.D.N. Buddhipala (Chief Financial Officer)

Mr. R. Rodrigo (Compliance Officer) - Until October 2015

Mr. C.J. Wijetillake (Compliance Officer) - Since November 2015

Mr. S.K.K. Hettihamu (Chief Risk Officer)

Mr. S.M.A. Jayasinghe (Consultant to BAC) attended 8 out of the 10 meetings held during the year.

Composition of the Main Board and Board Sub-Committee Composition as at December 31, 2015

| Gender | Age Group | |||||||

| Name of Committee | Executive Members | Non-Executive Members | Independent Members | Non-Independent Members | Male | Female | Below 50 Years | Over 50 Years |

| Main Board | 2 | 6 | 6 | 2 | 8 | Nil | Nil | 8 |

| Board Audit Committee | 2* | 3 | 3 | 2 | 5 | Nil | Nil | 5 |

| Board Integrated Risk Management Committee | 2** | 3 | 3 | 2 | 5 | Nil | Nil | 5 |

| Board Nomination Committee | 1* | 3 | 3 | 1 | 4 | Nil | Nil | 4 |

| Board Human Resources and Remuneration Committee | 1* | 3 | 3 | 1 | 4 | Nil | Nil | 4 |

| Board Credit Committee | 2 | 2 | 2 | 2 | 4 | Nil | Nil | 4 |

| Board Technology Committee | 2 | 1 | 1 | 2 | 3 | Nil | Nil | 3 |

| Board Investment Committee | 2 | 3 | 3 | 2 | 5 | Nil | Nil | 5 |

| Board-Related Party Transactions Review Committee | 2 | 2 | 2 | 2 | 4 | Nil | Nil | 4 |

Table - 5

* Attended by invitation

** One member attended by invitation

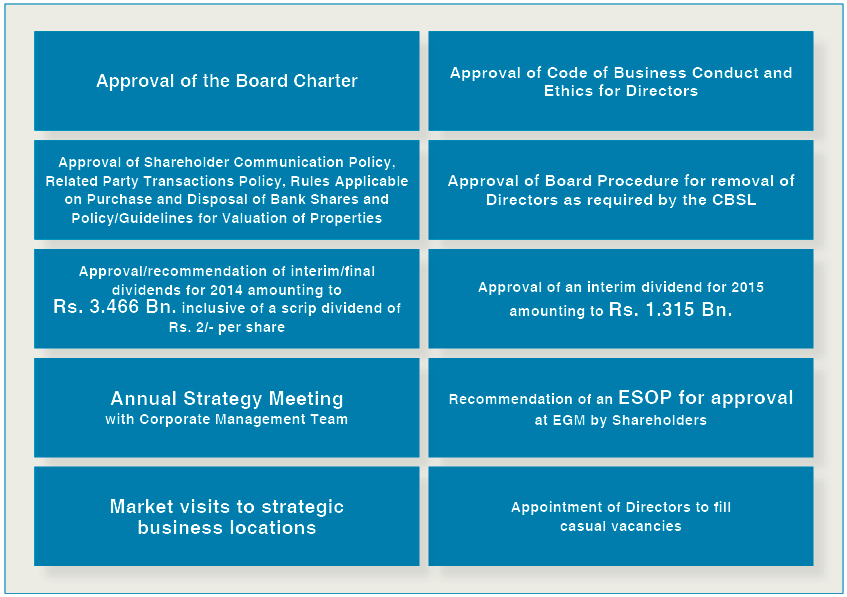

Major Initiatives of Board in 2015

Management Committees

Executive Committees also have been established by the Board to facilitate sufficient deliberation, co-operation across departments and healthy debate on matters considered as critical for the Banks operations as described below (Table 6):

| Management Committees | Purpose and tasks | Composition |

| Executive Integrated Risk Management Committee (EIRMC) | Monitors and reviews all risk exposures and risk related policies and procedures affecting credit, market and operational areas in line with the directives from the BIRMC |

CEO, COO and key members of the Risk Management, Personal Banking, Corporate Banking, Treasury, Inspection/Internal Audit, Compliance and Finance Departments. |

| Assets & Liabilities Committee (ALCO) | Optimises the Banks financial goals whilst maintaining liquidity and managing exposure to market risk within the Banks pre-determined risk appetite. | CEO, COO and key members of the Treasury, Corporate Banking, Personal Banking, Risk Management and Finance Departments. |

| Credit Policy Committee (CPC) | Reviews and approves credit policies and procedures pertaining to the effective management of all credit portfolios within the lending strategy of the Bank. | CEO, COO and key members of the Corporate Banking, Personal Banking, Risk Management, Inspection, Recoveries, and Branch Credit Monitoring Departments. |

|

Executive Committee on Monitoring NPAs (ECMN) |

Reviews and monitors the Banks Non-Performing Advances (NPAs) to initiate timely corrective action to prevent /reduce credit losses to the Bank. | CEO, COO and key members of the Corporate Banking, Personal Banking, Recoveries and Risk Management Departments. |

| Business Continuity Management Steering Committee (BCMSC) | Directs, guides and oversees the activities of the Business Continuity Plan of the Bank in accordance with the Banks strategy. | COO and key members of the Banks Corporate Management covering all business lines. |

| Information Security Council (ISC) | Continuous focus on meeting the information security objectives and requirements of the Bank. | Key members of the Risk, Information Systems Audit, Operations and IT Departments. |

| Investment Committee | Oversees the investment activities by providing guidance to the management | CEO, COO and key members of the Treasury and Finance Departments. |

| Human Resources Steering Committee (HRSC) | Makes recommendations to BHRRC on policy matters covering formulation of compensation packages, changes to organisational structure, developing a talent pipeline and staff promotions. | CEO, COO and key member of the HR, Corporate Banking, Personal Banking and Finance Departments. |

Table - 6

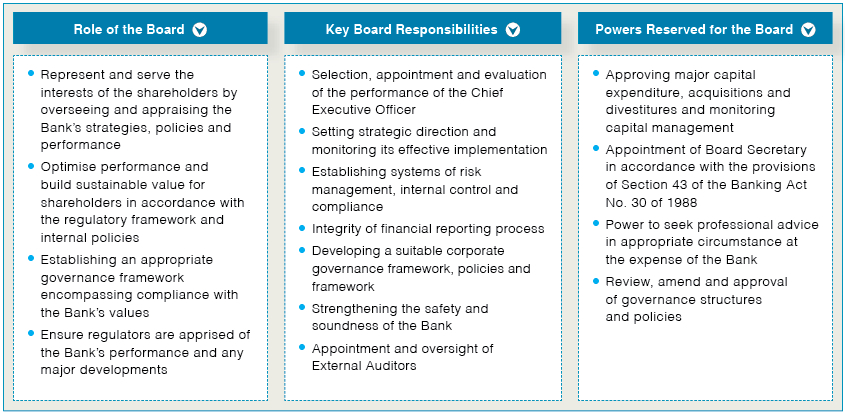

Board Responsibilities (Principle A 1.2.)

Responsibilities of the Board are set out in the Board Charter which includes a schedule of powers reserved for the Board (Figure 8).

Figure - 8

The Board provides guidance in formulating the Banks 5 year strategic plan which is prepared and presented by the Corporate Management to the Board who reviews and approves the same at a Special Board meeting convened for the purpose. Performance vis-à-vis the strategic plan is monitored at monthly Board meetings whilst specialised areas identified for oversight by Board

Sub-Committees have been monitored and progress and concerns reported to the Board.

The Board is assisted by the following Sub-Committees in fulfilling their role as set out in the Code:

- The BNC supports the Board in ensuring that the MD and other KMP have the necessary skills, experience and knowledge to implement strategy and also reviews succession plans for the Bank and for the MD and KMP.

- The BAC assists the Board in ensuring effective systems to secure integrity of information, internal controls and adopting appropriate accounting policies and fostering compliance with financial regulation.

- The BIRMC supports the Board on management of risk and ensuring compliance with laws and regulations. The BIRMC is supported by the

Banks Risk Management and Compliance functions. - The BHRRC is tasked with review of the Banks Code of Ethics which clearly communicates the ethical standards expected of all employees and Directors. The Code provides explicit guidance in ensuring that all stakeholder interests are considered in corporate decisions involving remuneration policy and

fosters a compliance culture with

respect to financial regulations and the Banks internal policy frameworks including accounting policies and sustainability policies. - Other Committees of the Board comprising BTC, BCC, BRPTRC and BIC assist the Board with specific aspects critical to the business operations of the Bank.

Act in Accordance with Laws (Principle A.1.3)

The Board has an approved Working Procedure in place to facilitate compliance with the relevant laws, CBSL directions and guidelines and international best practice with regard to the operations of the Bank. This includes provision to obtain independent professional advice as and when necessary, co-ordinated through the Company Secretary. Independent professional services were sought on matters in accordance with the above provision in 2015, on 09 occasions for which the expenses were borne by the Bank.

Access to advice and services of Company Secretary (Principle A.1.4)

All Directors are able to obtain the advice and services of the Company Secretary and the appointment and removal of the Company Secretary are matters involving the whole Board under recommendation of the BNC as it is a Key Management Position. The Company Secretarys responsibilities are summarised below:

- Matters pertaining to the conduct of Board Meetings and General Meetings;

- Conduct of proceedings in accordance with the Articles of Association and relevant legislation;

- Co-ordinating the publication and distribution of the Banks Annual Report;

- Maintaining registers of shareholders, company charges, Directors and secretary, Directors interests in shares and debentures, interests in voting shares, debenture holders, interests register and the seal register;

- Filing statutory returns/information with the Registrar of Companies;

- Adoption of best practice on corporate governance including facilitating and assisting the Directors with respect to their duties and responsibilities, in compliance with relevant legislation and best practice;

- Acting as a channel of communication and information for Non-Executive Directors and shareholders;

- Disclosures on related parties and related party transactions as required by laws and regulations;

- Monitoring and ensuring compliance with the listing rules and managing relations with the CSE through the Banks brokers;

- Assisting the Board in implementing and administering Directors and employees share participation schemes;

- Obtaining legal advice in consultation with the Board on company law, SEC, CSE and other relevant legislations in ensuring that the Company complies with all applicable laws and regulations.

Independent judgement (Principle A.1.5)

The Board comprises of senior professionals who are luminaries in their respective fields and collectively contribute their skills, perspectives and experience to the Board enriching the discussion and debate on matters set before them. As experienced professionals, they use their independent judgement on issues of strategy, performance, resources, key appointments and standards of business conduct. The composition of the Board ensures that there is a sufficient balance of power and contribution by all Directors and minimises the tendency for one or few members of the Board to dominate the Board processes or decision-making.

Dedicate Adequate Time and Effort to Matters of the Board and the Company (Principle A.1.6)

Board meetings and Board Sub-Committee meetings are scheduled well in advance and the relevant papers are circulated a week prior to the meeting using electronic means to ensure that Directors have sufficient time to review the same and call for additional information or clarifications, if required. While there is provision to circulate board papers closer to the meeting, in exceptional circumstances, this is generally discouraged. Members of the Corporate Management and external experts make representations to the Board and Board Sub-Committees on the business environment, regulatory changes, operations and other developments on a regular basis to facilitate enhancing the knowledge of the Board on matters relevant to the Banks operations.

It is estimated that Non-Executive Directors dedicate not less than 12 days per annum for the affairs of the Bank and those Directors who serve on BAC and BIRMC dedicate a further 4 days each for the affairs of the Bank.

Training for Directors (Principle A.1.7)

On appointment, Directors are provided with access to the electronic support system, which can archive minutes for the past 2 years and an induction pack which comprises the Articles of Association, Banking Act Directions, Directors Handbook published by the Sri Lanka Institute of Directors, Code of Best Practice on Corporate Governance, the Banks organisational structure, Board Charter and the most recent Annual Report. All Directors are encouraged to obtain membership of the Sri Lanka Institute of Directors which conducts a robust programme to support Directors. It is mandatory for the Directors to attend Director Forums organised by the CBSL. As stated above, Corporate Management and external experts make regular presentations with regard to the business environment in relation to the operations of the Bank.

Division of Responsibilities between the Chairman and CEO (Principle A.2)

The positions of the Chairman and the CEO have been separated in-line with best practice in order to maintain a balance of power and authority. The Chairman is a Non-Executive Director whilst the CEO is an Executive Director appointed by the Board. The roles of the Chairman and the CEO are clearly defined in the Board Charter.

The Chairmans Role (Principle A.3)

The Chairman provides leadership to the Board, preserving order and facilitating the effective discharge of the duties of the Board and is responsible for ensuring the effective participation of all Directors and maintaining open lines of communication with KMP, acting as a sound Board on strategic and operational matters. The agenda for Board Meetings are determined by the Chairman in consultation with the Company Secretary and Directors wishing to include items on the agenda may request the Chairman to discuss the same.

Financial Acumen (Principle A.4)

The Chairman of the BAC and the Deputy Chairman are both Fellow members of the CASL ensuring a sufficiency of financial acumen within the Board on matters of finance. The Chairman is a former Deputy Governor of the CBSL. Additionally, other Directors on the Board are luminaries in their respective fields with sufficient financial acumen.

Board Balance (Principle A.5)

The Board comprises 6 Non-Executive Directors and 2 Executive Directors facilitating an appropriate balance within the Board. All Non-Executive Directors are independent of management and free of business dealings that may be perceived to interfere with the exercise of their unfettered and independent judgement. They submit annual declarations to this effect which are evaluated to ensure compliance with the criteria for determining independence which are based on the requirements of the Code.

The Chairman holds a meeting at least once a year with only the Non-Executive Directors without the presence of the Executive Directors. Directors concerns regarding matters which are not resolved unanimously are recorded in the minutes.

There was one Alternate Director during the year. Except for the appointment of that Alternate Director, there were no circumstances which warranted appointment of Alternate Directors or a ‘Senior Director as the roles of the Chairman and CEO are clearly segregated.

Supply of Relevant Information (Principle A.6)

Board members receive information regarding matters set before the Board, 7 days prior to the meetings and the Chairman ensures that all Directors are properly briefed on same by requiring the presence of KMP, when deemed necessary. Management also makes presentations on regular agenda items to the Board and its Sub-Committees. Additionally, the Directors have access to KMP, to seek clarifications or additional information on matters presented to the Board. Directors who are unable to attend a meeting is updated on proceedings through formally documented minutes which are also discussed at the next meeting to ensure follow up and proper recording.

Appointments to the Board and Re-Election (Principles A.7)

The BNC is responsible for setting in place a formal and transparent procedure for the appointment of new Directors and further information regarding the operations of this committee are given on this report. They receive resumes of the potential candidates recommended by the Board in the event of a vacancy of a Non-Executive Director and review same in order to make recommendations to the Board which may include an interview with the candidate. The process for appointment of Executive Directors is similar with the exception being that candidates are selected from amongst the KMPs, of the Bank. The BNC also assesses annually the combined knowledge and experience of the Board in relation to the Banks strategic plans to identify additional requirements which are addressed when incumbent Directors come up for re-election. Appointments of new Directors are promptly communicated to the CSE and shareholders through press releases, subsequent to obtaining approval from the CBSL. The communications typically includes a brief resume of the Director, relevant expertise, key appointments, shareholding, directorships in other entities and whether he is independent.

Re-Election (Principle A.8)

Two directors will offer themselves for re-election at each Annual General Meeting (AGM). The two longest serving Non-Executive Directors offer themselves for re-election at each AGM in rotation with the period of service being considered from the last date of appointment. If there are more than two Directors who qualify for re-election, the Directors may decide amongst themselves or draw lots to determine the Directors who will offer themselves for re-election. If a Director has been appointed as a result of a casual vacancy that has arisen since the previous AGM, that Director will offer himself for re-election at the next AGM. Prof. A.K.W. Jayawardane and Mr. K. Dharmasiri were appointed during the year to fill casual vacancies and are offering themselves for re-election at the AGM to be held on March 31, 2016.

Appraisal of Board Performance (Principle A.9)

The Board and its Sub-Committees annually appraise their own performances to ensure that they are discharging their responsibilities satisfactorily in accordance with the Board Charter, which includes the responsibilities set out in the Code and the Banking Act Direction No.11 of 2007.This process requires each Director to fill a Board Performance Evaluation Form, which incorporates all criteria specified in the Board Performance Evaluation Checklist of the Code. The responses are collated by the Company Secretary and submitted to the BNC and discussed at a Board Meeting.

Disclosure of Information in Respect of Directors (Principle A.10)

Information specified in the Code with regard to Directors are disclosed in this Annual Report as follows:

- Name, qualifications, expertise, material business interests, key appointments and brief profiles on this report.

- Other business interests.

- Membership of committees, status of Directors attendance at Board Meetings and Board Sub-Committee meetings are on Table 3 - 5.

- Remunerations under Note 20 to the Financial Statements.

Appraisal of CEO (Principle A.11)

The Board agree the criteria for assessing performance with the CEO at the beginning of the year and assess performance based on same at the close of the financial year. The evaluation is formally approved within 4 months of the close of the financial year. This takes in to account performance vis-à-vis the targets, the operating environment and considers explanations provided for areas where performance has been below agreed targets. The Board is supported by the BHRRC in this process.

Directors Remuneration

Directors and Executive Remuneration (Principle B.1)

The BHRRC is responsible for making recommendations to the Board regarding the remuneration of Executive Directors. This vital committee comprises entirely of Non-Executive Directors who also meet the criteria for independence as set out in the Code. They consult the Chairman and the CEO regarding the same and also seek professional advice whenever deemed necessary. Remuneration for Non-Executive Directors is set by the Board as a whole. Remuneration for Executive Directors is set with reference to the Remuneration and Benefit Policy. The above processes ensure that no individual Director is involved in determining his or her own remuneration. The Board and the BHRRC engage the services of HR professionals on a regular basis to assist in the discharge of their duties in this regard.

The Level and Make Up of Remuneration (Principle B2)

It is the responsibility of the BHRRC to ensure that the remuneration of both Executive and Non-Executive Directors is sufficient to attract eminent professionals to the Board and retain them as contributing members in driving the performance of the Bank. Remuneration and benefits of the Executive Directors and KMP, are determined in accordance with the remuneration policies of the Bank which are designed to be attractive, motivating and capable of retaining high performing, qualified and experienced employees in the Bank.

Remuneration and Benefit Policy

The Remuneration and Benefit Policy of the Bank is to articulate a distinctive value proposition for current and prospective employees that attracts and retains people with the capabilities and values that the employer needs to succeed and also to provide a framework from which the employer designs, administers and evaluates effective reward programmes with the maximum motivational impact to drive desired behaviours and results.

The key elements of the rewards strategy based on the Remuneration and Benefit Policy is given below and the rewards strategy for the Bank will address each of the above points in alignment with the Banks overall business and people strategy.

- Pay philosophy - the overarching principles on which salaries and benefits are designed.

- Pay approach - the definition of various anchors of compensation and their role.

- Pay positioning - the external competitiveness of an organisations salaries and benefits programme.

- Pay parity - the Bank's stance on internal equity as opposed to external competitiveness.

- Pay delivery - the actual method in which salaries and benefits are communicated and delivered to employees.

- Pay mix - the ratio between fixed and variable pay given to employees at various levels in the organisation.

Total remuneration of KMP, is made-up of three components, namely guaranteed remuneration and variable remuneration which comprises an annual performance bonus and Employee Share Option Plan (ESOP). The BHRRC seeks the assistance of professionals in structuring the remuneration and benchmarking with market on a regular basis to ensure that total remuneration levels remain competitive in order to attract and retain key talent whilst balancing the interests of the shareholders. It also takes into consideration the views of the Banks two employee associations - the Executive Association and the Ceylon Bank Employees Union with whom it maintains a regular dialogue.

Guaranteed pay includes the monthly salary and allowances which are determined with reference to the qualifications, experience, levels of competencies, skills, roles and responsibilities of each employee. These are reviewed on an annual basis and adjusted for promotions, performance and inflation. The annual performance bonus is determined with reference to a multi-layered performance criteria matrix which is clearly communicated to the relevant categories of employees. The ESOP approved by the shareholders at the AGM held on March 31, 2015 is also part of the performance related remuneration for Executive Officers in Grade 1A or above.

Refer Note 52 to the Financial Statements on ‘Share-based payment.

There are no compensation commitments in employment contracts for early terminations and there were no instances of early termination during the year that required compensation.

The remuneration for Non-Executive Directors is fixed by the Board as a whole based on the recommendations of the BHRRC at a level in line with rates prevailing in the market, taking into account the time, commitments and responsibilities of their roles. Non-Executive Directors are not eligible for share ownership plans of the Bank.

Disclosure of Remuneration (Principle B.3)

The remuneration policy is disclosed on this section and the Report of the BHRRC conforms to Schedule D - Specimen Remuneration Committee Report. The names of the BHRRC members are set out on this report and the aggregate remuneration paid to Executive and Non-Executive Directors is given in Note 20 to the Financial Statements.

Relations with Shareholders

Constructive use of the AGM (Principle C.1)

The Bank had over 8,000 voting shareholders of whom approximately 73% exercised their rights to vote by attending the AGM or by proxy. The AGM provides a forum for all shareholders to participate in decision-making matters reserved for the shareholders which typically include proposals to adopt the Annual Report and Accounts, Appointment of Directors and Auditors and other matters requiring special resolutions as defined in the Articles of Association or the Companies Act No. 07 of 2007. The Chairman ensures the presence of the Chairman of the BAC, BHRRC and BNC to respond to any questions that may be directed to them by the Chairman. Notice of the AGM is circulated 15 working days in advance together with the Annual Report and Accounts which includes information relating to any other resolutions that may be set before the shareholders at the AGM.

Communication with Shareholders (Principle C.2.)

A Shareholder Communication Policy was approved during the year to clearly define how the Bank will engage with shareholders and the investment community at large codifying its current practices which are in compliance with the Companies Act, SEC and CSE requirements and the Code of Best Practice on Corporate Governance.

The Bank has multiple channels of communication with its shareholders which include a dedicated investor relations website at www.combank.lk/newweb/investor-relations, press releases and notices in English, Sinhala and Tamil newspapers and required disclosures to the CSE which are published on the CSE website. The Interim Financial Statements are published in the English, Sinhala and Tamil newspapers within 45 days except in the fourth quarter in which it is done within two months as required by the Directions of the CBSL. It is also the intention of the Board to ensure that the Annual Report provides a balanced review of the Banks performance which is comprehensive but concise.

Major & Material Transactions (Principle C.3)

There were no transactions which would materially alter the Banks or Groups net asset base nor any major related party transactions apart from those disclosed in the Directors Report and Note 62 to the Financial Statements.

Accountability and Audit

Financial Reporting (Principles D.1)

The Annual Report presents a balanced review of the Banks financial position, performance and prospects which have been presented combining both narrative and visual elements to ensure that the content is understandable. Care has been exercised to ensure that all statutory requirements are complied with in the Annual Report and in the issue of interim communications on financial performance which are reviewed by the Audit Committee and approved prior to publication. The following disclosures as required by the Code are included in this Report:

- Annual Report of the Board of Directors includes the disclosures required as per Principle 1.3 of the Code

- Statement of Directors Responsibility contains a statement setting out the responsibilities of the Board for the preparation and presentation of Financial Statements

- Independent Auditors Report includes a statement of their responsibilities

- Directors Statement on Internal Control.

- ‘Focus on Value Creation which discusses the reviews traditionally included under ‘Management Discussion and Analysis

- Statement of going concern of the Company is set out in item (m) in the Statement of Directors Responsibility and Item 19 of the Annual Report of the Board of Directors.

- Related Party Transactions are disclosed in Item 14 of the Directors Report and in Note 62 in the Financial Statements and the process in place is described in the Report of the BRPTRC.

In the unlikely event of the net assets of the Company falling below 50% of Shareholders Funds the Board will summon an Extraordinary General Meeting to notify the shareholders of the position and to explain the remedial action being taken. The Financial Statements clearly explain the movement of net assets during the year. Refer this section for details.

Internal Control and Audit Committee (Principle D.2 & 3)

The Board is responsible for formulating and implementing appropriate processes for risk management and internal control systems to safeguard shareholder interests and assets of the Bank. BIRMC assists the Board in discharge of its duties with regard to risk management and the BAC assists the Board in discharge of its duties in relation to internal controls. Their responsibilities are summarised in the respective Committee reports appearing under Board Sub-Committee Reports section and have been formulated with reference to the requirements of the Code, the Banking Act Direction No.11 of 2007 on Corporate Governance and the Banks business needs. The BIRMC is supported by the Integrated Risk Management Department of the Bank and a comprehensive report of how the Bank manages risk is included on this report and the Committees report on Board Sub-Committee Reports section.

The BAC comprises 3 Independent Non-Executive Directors and a summary of its responsibilities and activities are given in the Report of the BAC. It is supported by the Internal Audit function of the Bank who report directly to the Audit Committee. The Chairman of the BAC is Mr. S. Swarnajothi, a Fellow member of CASL and a former Auditor General of Sri Lanka. The Committee has also appointed Mr. Manil Jayesinghe FCA, FCMA, Partner of Ernst & Young as a Consultant to the BAC and is invited to the meetings. The Board also obtains assurance from its External Auditors on the effectiveness of internal controls on financial reporting.

Code of Business Conduct & Ethics and Corporate Governance Report (Principles D.4 & D.5.)

The Bank has an internally developed Code of Conduct and Business Ethics which is applicable to all employees. The Bank also has Board adopted rules applicable on Commercial Bank Share Purchases/Disposals by the Board of Directors of the Bank in terms of CSE Listing Rules.

The Code of Business Conduct and Ethics is in compliance with the requirements of the Schedule I of the Code of Best Practice on Corporate Governance. The BHRRC reviews the Code of Business conduct and Ethics to ensure that it is sufficient and relevant with reference to the current operations of the Bank.

This Section on ‘How We Govern complies with the requirement to disclose the extent of compliance with the Code of Best Practice on Corporate Governance as specified in Principle D5.

Shareholders

Shareholder Relations (Principles E & F)

The Bank has 9,412 voting ordinary shareholders of which 6% are institutional shareholders. We have a regular structured dialogue with the large institutional shareholders and any concerns of these institutional shareholders expressed at the meetings is communicated to the Board as a whole. All shareholders are encouraged to exercise their voting powers at the AGM. We also facilitate the analysis of the securities of the Bank by encouraging both foreign and local analysts covering the Bank with structured meetings where they are able to obtain information and explanations required for evaluating the current and future performance of the Company, sector and country. Additionally, the Investor Relations page on the Banks website has key information required by shareholders and analysts.

Sustainability

Sustainability Reporting (Principle G)

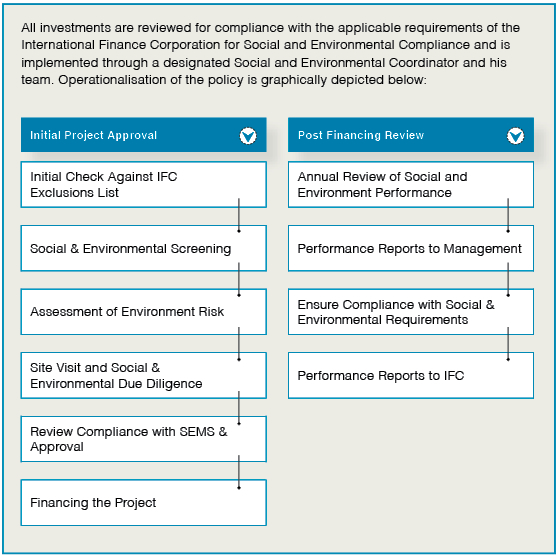

The Bank is an early champion of sustainability and sustainability reporting based on GR2 Guidelines commenced in 2009, Sustainability principles are embedded in our business operations through the SEMS Policy, considered in formulating our business strategy and reported in a holistic manner throughout this Report.

The Bank takes in to account ‘The Rio Declaration on Environment and Development, 1992. ‘Principle 15: in operationalising its SEMS policy which states that ‘In order to protect the environment, the precautionary approach shall be widely applied by States according to their capabilities. Where there are threats of serious or irreversible damage, lack of full scientific certainty shall not be used as a reason for postponing cost-effective measures to prevent environmental degradation. Accordingly, the Bank has a list of prohibited industries to which financial accommodation or investments are not considered.

Information required by the Code is located as follows:

Principle 1 - Reporting of Economic Sustainability - Financial Capita.

Principle 2 - Reporting on the Environment - Impact on Environment.

Principle 3 - Reporting on Labour Practices - Human Capital.

Principle 4 - Reporting on Society - Social Impact.

Principle 5 - Reporting on Product Responsibility - Social and Network Capital.

Principle 6 - Reporting on Stakeholder Identification, Engagement and Effective Communication - Stakeholder Engagement.

Principle 7 - Sustainable Reporting to be formalised as part of the reporting process and to take place regularly - About this Report.

Banks Social & Environmental Management System

Figure - 9

The Banking Act Direction No.11 of 2007 and subsequent amendments thereto on Corporate Governance for Licensed Commercial Banks in Sri Lanka issued by the CBSL

| Section | Principle | Compliance and Implementation | Complied | ||||||||||||||||||

| 3 (1) | Responsibilities of the Board | ||||||||||||||||||||

| The Board has strengthened the safety and the soundness of the Bank in the following manner: | |||||||||||||||||||||

| a. |

Setting strategic objectives and corporate values |

The Banks strategic objectives and corporate values are determined by the Board and are given on Figure 1. These are communicated to all levels of staff through budgets, structured meetings and reinforced through quarterly review meetings which review performance vis-à-vis strategic goals.

Corporate values are included in the Code of Conduct and Business Ethics which is provided in a booklet to all employees and also available on the intranet. |

✓ | ||||||||||||||||||

| b. |

Approving overall Business Strategy including Risk Management Policy |

The Board provided direction and guidance for preparation of the 5 year Corporate Plan from 2015 – 2019 which was approved by the Board at the beginning of the year after discussing related issues in detail with the Corporate Management. The Corporate Plan has been aligned to the overall Risk Strategy of the Bank through the involvement of BIRMC. The risk appetite of the Bank is embedded throughout the Corporate Plan in allocation of capital, adoption of risk matrix to measure the risk levels and in defining key performance indicators which include both quantitative and qualitative criteria. Additionally, governance and compliance embedded into Bank wide Risk Management Policy Framework and are included in the strategic goals. The Banks Corporate Plan for 2016-2020 was approved on January 29, 2016 by the Board. | ✓ | ||||||||||||||||||

| c. | Risk management | The BIRMC is tasked with making recommendations to the Board on the Banks Risk Management Policy, defining the risk appetite, identifying principal risks, setting governance structures and implementing systems to measure, monitor and manage the principal risks. The Section on ‘Managing Risk at Commercial Bank and the BIRMC Report provide further insights on Risk Management Policies and processes of the Bank. | ✓ | ||||||||||||||||||

| d. | Communication with all stakeholders |

The Board has approved and implemented the following communication policies:

|

✓ | ||||||||||||||||||

| e. | Internal Control System and Management Information Systems |

The Board is assisted in this regard by the BAC who review the adequacy and the integrity of the Banks Internal Control System and Management Information System. The BAC has reviewed reports from the Internal Audit Department and the External Auditors in carrying out this function and reviewed management responses on the same during the year.

Internal Audit Department also carries out Information Systems Audits to assess the effectiveness of the Management Information System. |

✓ | ||||||||||||||||||

| f. | Key Management Personnel (KMP) |

KMP are defined in the Sri Lanka Accounting Standards, who significantly influence policy, direct activities and exercise control over business activities, operations and risk management. In addition, the officers with designation identified in the guidelines are included as KMP for Corporate Governance reporting purpose. All appointments of designated KMP are recommended by the BNC and approved by the Board.

Further, for Corporate Governance reporting and monitoring purposes, the Bank has included selected members of the Corporate Management in addition to the KMP identified for financial reporting purposes. |

✓ | ||||||||||||||||||

| g. | Define areas of authority and key responsibilities for Directors and KMP | The Board Charter sets out the matters specifically reserved for Board, defining the areas of authority and key responsibilities of the Board of Directors. Areas of authority and key responsibilities for members of the Corporate Management are stated in the Job Descriptions of each member. | ✓ | ||||||||||||||||||

| h. |

Oversight of affairs of the Bank by KMP |

The Board reviews the performance of the Bank vis-à-vis the Strategic Plan and receives reports from its Sub-Committees on financial reporting, internal control, risk management, changes in KMP and other relevant matters delegated to them. Additionally, KMP make regular presentations to the Board on matters under their purview and are also called in by the Board to explain matters relating to their areas. | ✓ | ||||||||||||||||||

| i. | Assess effectiveness of own Governance Practices | Completed Board Evaluation Forms were received from all Board members for 2015 and the responses were discussed at a BNC Meeting and a subsequent Board meeting. Matters of concern noted are followed-up and improved upon during the year to uphold the good governance practices of the Bank. | ✓ | ||||||||||||||||||

| j. | Succession plan for KMP | There is a formal succession plan in place with named successors for KMP together with development plans to ensure their readiness. The succession plan for the CEO and KMP was reviewed by the BNC and approved by the Board during 2015. | ✓ | ||||||||||||||||||

| k. | Regular meetings with KMP | Progress towards corporate objectives is a regular agenda item for the Board and KMP are regularly involved in the Board level discussions on same. Additionally, they make presentations on key agenda items or are called in for discussions at the meetings of the Board and its Sub-Committees on policy and other matters relating to their areas on a regular basis. | ✓ | ||||||||||||||||||

| l. | Regulatory environment and maintaining an effective relationship with regulator | Directors are briefed about regulatory developments at Board meetings by the KMP to facilitate effective discharge of their responsibilities. Members of BAC and the BIRMC are also briefed on regulatory developments at their meetings by the Heads of Internal Audit, Risk and Compliance. All Board members attend the Director forums arranged by the CBSL as well. | ✓ | ||||||||||||||||||

| m. | Hiring External Auditors | The Board has adopted a Policy of Rotation of Auditors, once in every 5 years, in keeping with the principles of Good Corporate Governance. At the end of the 5-year period, quotations are called from suitable audit firms, prior to the recommendation of new Auditors as per the rotation policy. In addition to this, External Auditors submit a statement annually confirming their independence as required by Section 163 (3) of the Companies Act No. 07 of 2007 in connection with external audit. | ✓ | ||||||||||||||||||

| 3 (1) (ii) | Appointment of Chairman and CEO and defining and approving their functions and responsibilities | Positions of the Chairman and the CEO are separated in the Board Charter to maintain a balance of power. Further, functions and responsibilities of the Chairman and the CEO are properly defined and approved in line with Direction 3 (5) of these Directions. | ✓ | ||||||||||||||||||

| 3 (1) (iii) | Regular Board Meetings | Regular monthly Board meetings are held on the last Friday of each month and special meetings are scheduled as and when the need arises at which Directors present actively participate in deliberating matters set before the Board. Attendance at Board meetings is given on Table 4. together with the number of meetings of the Board and its Sub-Committees. We have minimised obtaining approval via circular resolutions and it is done only on an exceptional basis and such resolutions are tabled at the next Board meeting for record purpose. | ✓ | ||||||||||||||||||

| 3 (1) (iv) |

Arrangements for Directors to include proposals in the agenda |

Notice of Meeting is circulated one week prior to the meeting and Directors may submit proposals for inclusion in the agenda on discussion with the Chairman on matters relating to the business of the Bank. |

✓ | ||||||||||||||||||

| 3 (1) (v) | Notice of Meetings | Notice of Meetings, agenda and Board Papers for the Board meetings are circulated to the Directors 07 days prior to the meeting giving Directors time to attend and submit any urgent proposals. | ✓ | ||||||||||||||||||

| 3 (1) (vi) | Directors attendance | The Directors are apprised of their attendance in accordance with the Articles of the Company and the Corporate Governance Code. Detail of the Directors attendance is set out on this Table. No Director has been absent from 3 consecutive meetings and all Directors have attended at least 93% or 13 out 14 of the meetings. | ✓ | ||||||||||||||||||

| 3 (1) (vii) |

Appointment and setting responsibilities of the Company Secretary |

An Attorney-at-Law functions as the Secretary of the Board and she has taken steps to duly comply with the requirements under the Banking Act No. 30 of 1988. She has also ensured that proper Board procedures are followed and that applicable rules and regulations are adhered to. | ✓ | ||||||||||||||||||

| 3 (1) (viii) | Directors access to advice and services of Company Secretary | All Board members have full access, to the advice and services of the Company Secretary to ensure that proper Board procedures are followed and all applicable rules and regulations are complied with. | ✓ | ||||||||||||||||||

| 3 (1) (ix) | Maintenance of Board minutes | Company Secretary maintains the minutes of the Board meetings and circulates same to all Board members after review by the CEO and Chairman. The minutes are reviewed and approved at the next Board meeting after incorporating any amendments/inclusions proposed by other Directors. Additionally, the Directors have access to the past Board Papers and minutes through a secure electronic link. | ✓ | ||||||||||||||||||

| 3 (1) (x) |

Minutes to be of sufficient detail and serve as a reference for regulators and supervisory authorities |

The minutes of the meetings include:

|

✓ | ||||||||||||||||||

| 3 (1) (xi) | Directors ability to seek independent professional advice | Directors are able to obtain independent professional advice, as and when necessary, in discharging their responsibilities according to a procedure approved by the Board. This function is co-ordinated by the Company Secretary. | ✓ | ||||||||||||||||||

| 3 (1) (xii) |

Dealing with Conflicts of Interest |

The Directors make declarations of their interests at appointment, annually and whenever there is a change in the same and a quarterly report is sent to the Board on possible areas of conflict (if any). Directors abstain from participating in the discussions, voicing their opinion or approving in situations where there is a conflict of interest. Additionally such Directors presence is disregarded in counting the quorum in such instances. Key appointments of the Directors are included in their profiles. | ✓ | ||||||||||||||||||

| 3 (1) (xiii) | Formal schedule of matters reserved for Board decision | The Board has put in place systems and controls to facilitate the effective discharge of Board functions. Pre-set agenda of meetings ensures the direction and control of the Bank is firmly under Boards control and authority in line with regulatory codes, guidelines and international best practice. | ✓ | ||||||||||||||||||

| 3 (1) (xiv) | Informing Central Bank on solvency issues | The Bank is solvent and no situation arisen where its solvency has been in doubt. A Board approved procedures is in place to inform the Director of Banking Supervision prior to taking any decision or action if the Bank is about to become insolvent or about to suspend payments to its depositors and other creditors. | ✓ | ||||||||||||||||||

| 3 (1) (xv) |

Maintaining a sound Capital Adequacy |

The Board monitors capital adequacy and other prudential measures to ensure compliance with regulatory requirements, and the Banks defined risk appetite. The Bank is in compliance with the minimum capital requirements. | ✓ | ||||||||||||||||||

| 3 (1) (xvi) | Publish Corporate Governance Report in Annual Report | This Report forms part of the Corporate Governance Report of the Bank. | ✓ | ||||||||||||||||||

| 3 (1) (xvii) | Self-assessment of Directors | The Bank has adopted a system of self-assessment, to be undertaken by each Director, annually. Each member of the Board carried out a self-assessment of his/her own effectiveness as an individual as well as the effectiveness of the Board as a whole. Further, each Director carries out an assessment of ‘fitness and propriety to serve as a Director. | ✓ | ||||||||||||||||||

| 3 (2) | The Boards Composition | ||||||||||||||||||||

| 3 (2) (i) | Number of Directors | As per CBSL Governance Direction, the number of Directors should not be less than 07 nor more than 13. The Banks Board comprised 8 Directors as at December 31, 2015. | ✓ | ||||||||||||||||||

| 3 (2) (ii) | Period of service of a Director | The period of service of a Director is limited to 9 years excluding the Chief Executive Officer as per the Corporate Governance Code for Licensed Commercial Banks. Details of their tenures of service are given on this section. | ✓ | ||||||||||||||||||

| 3 (2) (iii) | Board balance | There are 02 Executive Directors and 6 Non-Executive Directors which is compliant with the requirement to limit the number of Executive Directors to 1/3 of the total number of Directors. | ✓ | ||||||||||||||||||

| 3 (2) (iv) | Independent Non-Executive Directors | The Board has 6 Independent Non-Executive Directors which is well above the regulatory requirement who satisfy the criteria for determining independence. | ✓ | ||||||||||||||||||

| 3 (2) (v) | Alternate Independent Directors | There was one appointment of an Alternate Director during the year. However, there are no Alternate Directors as at the Reporting date. | ✓ | ||||||||||||||||||

| 3 (2) (vi) |

Criteria for Non-Executive Directors |

Non-Executive Directors are persons with proven track records and necessary skills and experience to bring independent judgment to bear on issues of strategy, performance and resources.

Directors nominate names of eminent professionals or academics from various disciplines to the BNC who peruse the profiles and recommend suitable candidates to the Board. |

✓ | ||||||||||||||||||

| 3 (2) (vii) | Composition of Non-Executive Directors | The requirement to have more than half the quorum as Non-Executive Directors is strictly observed throughout the year and it is noteworthy that 6 out of the 8 Board members as at the Reporting date are Non-Executive Directors. | ✓ | ||||||||||||||||||

| 3 (2) (viii) |

Identify Independent Non-Executive Directors and disclosures required in the Annual Report |

The Independent Non-Executive Directors are expressly identified as such in all corporate communications that disclose the names of Directors of the Bank. The composition of the Board, by category of Directors, including the names of the Chairman, Executive Directors, Non-Executive Directors and Independent Non-Executive Directors are given in Item 11.1. | ✓ | ||||||||||||||||||

| 3 (2) (ix) | Formal and transparent procedure for appointments to the Board | The Board has established a Nomination Committee (BNC) whose Terms of Reference comply with the specimen given in the Code of Best Practice on Corporate Governance. Accordingly, new Directors including the CEO and COO are appointed by the Board upon consideration of recommendations by the BNC. The Board has also developed a succession plan together with the BNC to ensure the orderly succession of appointments to the Board. | ✓ | ||||||||||||||||||

| 3 (2) (x) | Re-election of Directors filling casual vacancies | All Directors appointed to the Board are subject to re-election by shareholders at the first AGM after their appointment. | ✓ | ||||||||||||||||||

| 3 (2) (xi) | Communication of reasons for removal or resignation of a Director | Resignations of Directors and the reasons are promptly informed to the regulatory authorities and shareholders as per CSE requirements together with a statement confirming whether or not there are any matters that need to be brought to the attention of shareholders. | ✓ | ||||||||||||||||||

| 3 (2) (xii) | Prohibition of Directors/Employees to be appointed as Directors of another bank | The Board and the BNC take into account this requirement in their deliberations when considering appointments of Directors. None of the Directors are Directors or employees at any other bank. | ✓ | ||||||||||||||||||

| 3 (3) | Criteria to Assess Fitness and Propriety of Directors | ||||||||||||||||||||

| 3 (3) (i) | Age of Directors should not exceed 70 years | There are no Directors who are over 70 years of age. | ✓ | ||||||||||||||||||

| 3 (3) (ii) | Restriction on Directors holding positions in other entities | No Director holds directorships of more than 20 companies/entities/institutions inclusive of Subsidiaries or Associate Companies of the Bank. | ✓ | ||||||||||||||||||

| 3 (4) | Management Functions Delegated by the Board | ||||||||||||||||||||

|

3 (4) (i) 3 (4) (ii) 3 (4) (iii) |

Understand and study delegation arrangements Extent of delegation within appropriate limits Review delegation arrangements periodically | The Board reviews and approves the delegation arrangements of the Bank annually and ensures that the extent of delegation addresses the business needs of the Bank whilst enabling the Board to discharge their functions effectively. Consequently, the Board takes time to study and understand the delegation arrangements. In terms of Articles of Association of the Bank the Board is empowered to delegate its powers . | ✓ ✓ ✓ |

||||||||||||||||||

| 3 (5) | The Chairman and CEO | ||||||||||||||||||||

| 3 (5) (i) | Separation of roles | There is a clear separation of duties between the roles of the Chairman and the CEO, thereby preventing unfettered powers for decision-making being vested with one person. | ✓ | ||||||||||||||||||

| 3 (5) (ii) | Non-Executive Chairman and appointment of a Senior Independent Director | The Chairman is an Independent Non-Executive Director. | ✓ | ||||||||||||||||||

| 3 (5) (iii) |

Disclosure of identity of Chairman and CEO and any relationships with the Board members |

The identity of the Chairman and CEO are disclosed in the Annual Report. The Board is aware that there are no relationships whatsoever, including financial, business, family, any other material/relevant relationship between the Chairman and the CEO. Similarly, no relationships prevail among the other members of the Board. | ✓ | ||||||||||||||||||

| 3 (5) (iv) | Chairman to provide leadership to the Board |

Board approved List of Functions and Responsibilities of Chairman include, ‘Providing Leadership to the Board as a responsibility of the Chairman. The Boards Annual Assessment Form includes an area to measure the ‘Effectiveness of the Chairman in facilitating the effective discharge of Board functions.

All key and appropriate issues are discussed by the Board on a timely basis. |

✓ | ||||||||||||||||||

| 3 (5) (v) |

Responsibility for agenda lies with Chairman but may be delegated to Company Secretary |

The Company Secretary draws up the agenda for the meetings in consultation with the Chairman. | ✓ | ||||||||||||||||||

| 3 (5) (vi) | Ensure that Directors are properly briefed and provided adequate information |

The Chairman ensures that the Board is sufficiently briefed and informed regarding the matters arising at Board. The following procedures ensure this:

|

✓ | ||||||||||||||||||

| 3 (5) (vii) |

Encourage active participation by all Directors and lead when acting in the interests of the Bank |

This requirement is addressed in the Chairmans List of Functions and Responsibilities of the Chairman approved by the Board.

Self evaluation is carried out by the Board annually. |

✓ | ||||||||||||||||||

| 3 (5) (viii) |

Encourage participation of Non-Executive Directors and relationships between Non-Executive and Executive Directors |

Six members of the Board are Non-Executive Directors which creates a conducive environment for active participation by the Non-Executive Directors. Additionally, Non-Executive Directors chair the Sub-Committees of the Board providing further opportunity for active participation. |

✓ | ||||||||||||||||||

| 3 (5) (ix) | Refrain from direct supervision of KMP and executive duties | The Chairman does not get involved in the supervision of KMP or any other executive duties. | ✓ | ||||||||||||||||||

| 3 (5) (x) | Ensure effective communication with shareholders |

The Bank historically has active shareholder participation at the AGM. At the AGM the shareholders are given the opportunity to take up matters for which clarification is needed. These matters are adequately clarified by the Chairman and/or CEO and/or any other officer. |

✓ | ||||||||||||||||||

| 3 (5) (xi) | CEO functions as the apex executive in charge of the day to day operations | The day-to-day operations of the Bank has been delegated to the CEO. | ✓ | ||||||||||||||||||

| 3 (6) | Board Appointed Committees | ||||||||||||||||||||

| 3 (6) (i) | Establishing Board committees, their functions and reporting | The Board has established 8 committees with written terms of reference for each of which 4 are mandatory with the remainder appointed to meet the business needs of the Bank. Each committee has a Secretary to arrange the meetings and maintain minutes, records, etc., under the supervision of the Chairman of the committee. The Reports of the sub-committees are included under; The Chairpersons of the sub-committees are available at the AGM to clarify any matters that may be referred to them by the Chairman. | ✓ | ||||||||||||||||||

| 3 (6) (ii) | BAC | ||||||||||||||||||||

| a. | Chairman to be an Independent Non-Executive Director with qualifications and experience in accountancy and/or audit | Chairman of the Committee Mr. S. Swarnajothi is an Independent Non-Executive Director. He is a Fellow of CASL and CMA Sri Lanka a member of CMA of Australia. A former Auditor General of Sri Lanka, he has the required skills and experience to function effectively in this capacity. | ✓ | ||||||||||||||||||

| b. | Committee to comprise solely of Non-Executive Directors | All members of the BAC are Independent Non-Executive Directors. | ✓ | ||||||||||||||||||

| c. | Audit Committee functions |

In accordance with the Terms of Reference, BAC has made the following recommendations:

|

✓ | ||||||||||||||||||

| d. | Review and monitor External Auditors independence and objectivity and the effectiveness of the audit processes | The Board has adopted a policy of rotation of Auditors, once in every 5 years, in keeping with the principles of Good Corporate Governance. | ✓ | ||||||||||||||||||

| e. | Provision of non-audit services by External Auditor |

Following action is taken prior to the assignment of non-audit services to External Auditors by the Bank:

|

✓ | ||||||||||||||||||

| f. | Determines scope of audit |

The committee discussed the Audit Plan and scope of the audit with External Auditors to ensure that it includes:

co-ordinating activities with other Auditors. |

✓ | ||||||||||||||||||

| g. | Review financial information of the Bank |

BAC reviews the financial information of the Bank, in order to monitor the integrity of the Financial Statements of the Bank, its Annual Report, Interim Financial Statements prepared for disclosure, and the significant financial reporting judgements contained therein. The review focuses on the following:

|

✓ | ||||||||||||||||||

| h. | Discussions with External Auditor on interim and final audits | BAC discusses issues, problems and reservations arising from the interim and final audits with the External Auditor. The committee met on 2 occasions with the External Auditors without the Executive Staff of the Bank being present | ✓ | ||||||||||||||||||

| i. | Review of Management Letter and Banks response | BAC has reviewed the External Auditors Management Letter and the managements response thereto. | ✓ | ||||||||||||||||||

| j. | Review of internal audit function |

The Annual Audit Plan prepared by the Internal Audit Department is submitted to the BAC for approval. This plan covers the scope and resource requirement relating to the Audit Plan.

The services of five audit firms have been obtained to assist the Internal Audit Department to carry out the audit function. Prior approval of the BAC has been obtained in this regard. The committee reviewed the reports submitted by internal audit and ensures that appropriate action is taken on the recommendations of the Internal Audit Department. The Assistant General Manager – Management Audit who leads the Internal Audit Department, reports directly to the BAC and his performance appraisal is reviewed by the Audit Committee. BAC is kept apprised of terminations/resignations of senior internal audit staff members and recommend their appointment. The above processes ensure that audits are performed with impartiality, proficiency and due professional care. |

✓ | ||||||||||||||||||

| k. | Internal investigations | Major findings of internal investigations and managements responses thereto are reviewed by the BAC. It has also ensured that the recommendations of such investigations are implemented. | ✓ | ||||||||||||||||||

| l. | Attendees at Audit Committee meetings | The CEO, CFO, Assistant General Manager – Management Audit and a representative of the External Auditors normally attend meetings. Other Board members may also attend meetings upon the invitation of the committee. The committee met with the External Auditors without the Executive Directors being present on 2 occasions during the year. | ✓ | ||||||||||||||||||

| m. | Explicit authority, resources and access to information |

The Terms of Reference for the BAC includes:

|

✓ | ||||||||||||||||||

| n. | Regular meetings | The BAC has scheduled regular quarterly meetings and additional meetings are scheduled when required. Accordingly, the committee met 10 times during the year. Members of the BAC are served with due notice of issues to be discussed and the conclusions in discharging its duties and responsibilities are recorded in the Minutes of the meetings maintained by the Company Secretary. | ✓ | ||||||||||||||||||

| o. | Disclosure in Annual Report |

The Report of the BAC includes the following:

|

✓ | ||||||||||||||||||

| p. | Maintain minutes of meetings | Assistant General Manager – Management Audit serves as the Secretary of the BAC and maintains minutes of the committee meetings. | ✓ | ||||||||||||||||||

| q. |

Whistle-blowing policy and arrangements available for employees to raise concerns in confidence |

The Bank has a Whistle-blowing Policy which has been reviewed and approved by the BAC and the Board of Directors. Boards responsibility towards encouraging communication on any non-compliance and unethical practices were addressed in the Board Charter.

A process is in place and proper arrangements are in effect to conduct fair and independent investigation and appropriate follow up action regarding any concerns raised by the employees of the Bank, in relation to possible inappropriate financial reporting, internal controls or other matters. |

✓ | ||||||||||||||||||

| 3 (6) (iii) | BHRRC | ||||||||||||||||||||

| Charter of the Committee |

The Committee is responsible for:

|

✓ | |||||||||||||||||||

| 3 (6) (iv) | BNC | ||||||||||||||||||||

| a. |

Appointment of Directors, CEO and KMP |

The committee has developed and implemented a procedure to appoint new Directors, CEO and KMP.

The committee is chaired by the Chairman of the Bank and two other Independent Directors. The CEO may be present at meetings by invitation. Refer the BNC Report. |

✓ | ||||||||||||||||||

| b. | Re-election of Directors | The committee makes recommendations regarding the re-election of current Directors, taking into account the performance and contribution made by the Director concerned towards the overall discharge of the Boards responsibilities. | ✓ | ||||||||||||||||||

| c. | Eligibility criteria for appointments to key managerial positions including CEO | The committee sets the eligibility criteria to be considered, including qualifications, experience and key attributes, for appointment or promotion to key managerial positions including the position of the CEO. The committee considers the applicable statutes and guidelines in setting the criteria. | ✓ | ||||||||||||||||||

| d. | Fit and proper persons |

The committee obtains annual declarations from Directors and CEO to ensure that they are fit and proper persons to hold office as specified in the criteria given in Direction 3 (3) and as set out in the Statutes.

Further, the BHRRC obtains annual declaration from KMP to ensure that they too are fit and proper persons to hold office as specified in the said Direction. |

✓ | ||||||||||||||||||

| e. |

Succession Plan and new expertise |

The committee has developed a succession plan for the Directors whilst succession planning for KMP is carried out by the BHRRC. The BNC calls for few suitable CVs, check suitability with independent organisations and recommends to the Board.

The need for new expertise may be identified by the Board or its committees and brought to the attention of the BNC who will take appropriate action. |

✓ | ||||||||||||||||||

| f. | Committee to be chaired by an Independent Director | The Committee was chaired by an Independent Non-Executive Director and the CEO was present at the meeting by invitation. | ✓ | ||||||||||||||||||

| 3 (6) (v) | BIRMC | ||||||||||||||||||||

| a. | Composition | The committee comprises 3 Non-Executive Directors, CEO, CRO and CFO who serves as the Secretary to the committee. Other KMP supervising credit, market, liquidity, operational and strategic risk are invited to attend the meeting on a regular basis. | ✓ | ||||||||||||||||||

| b. | Risk Assessment | The committee has approved the policies on Credit Risk Management, Market Risk Management and Operational Risk Management which provides a framework for management and assessment of risks. Accordingly, monthly information on pre-established risk indicators are reviewed by the committee in discharging its responsibilities as per the Terms of Reference. | ✓ | ||||||||||||||||||

| c. | Review of management level committees on risk |

The committee reviews the reports of the management level CPC and the ALCO to assess their adequacy and effectiveness in addressing specific risks and managing the same within the quantitative and qualitative risk limits set in the Risk Appetite Statement approved by the Board on a regular basis.

Further, adequacy and effectiveness of all management level risk-related committees such as EIRMC, ALCO, CPC and ECMNs are reviewed by the BIRMC annually. |

✓ | ||||||||||||||||||

| d. |

Corrective action to mitigate risks exceeding prudential levels |

Actual exposure levels under each risk category are monitored against the tolerance levels when preparation of ‘Risk Profile Dashboard of the Bank which is circulated among members of the BIRMC on a monthly basis and discussed in detail at quarterly meetings.

The committee takes prompt corrective action to mitigate the effects of specific risks in the event such risks are at levels beyond the prudent levels decided by the committee on the basis of the Banks policies and regulatory and supervisory requirements. |

✓ | ||||||||||||||||||

| e. | Frequency of meetings | The committee has regular quarterly meetings and schedules additional meetings when required. The agenda covers matters assessing all aspects of risk management including updated business continuity plans. The committee met 4 times during 2015. | ✓ | ||||||||||||||||||

| f. | Actions against officers responsible for failure to identify specific risks or implement corrective action | Committee refers such matters, if any, to the Human Resources Department for necessary action. | ✓ | ||||||||||||||||||

| g. |

Risk Assessment Report to Board |

A Comprehensive Report of the meeting is submitted to the Board after each committee meeting by the Secretary of the Committee for their information, views, concurrence or specific directions. | ✓ | ||||||||||||||||||

| h. | Compliance function | A compliance function has been established to assess the Banks compliance with laws, regulations, regulatory guidelines, internal controls and approved policies on all areas of business operations. This function is headed by a dedicated Compliance Officer who reports to the BAC and the BIRMC. The Compliance Officer submits a Positive Assurance Certificate on Compliance with Mandatory Banking and Other Statutory Requirements on quarterly basis to the BAC and the BIRMC. | ✓ | ||||||||||||||||||

| 3 (7) | Related Party Transactions (RPT) | ||||||||||||||||||||

| 3 (7) (i) | Avoid conflict of interest |

The BRPTRC is tasked with oversight of the processes relating to this subject.

All members of the Board are required to make declarations of the positions held with related parties at the time of appointment and annually thereafter. This information is provided to the Finance Division enabling them to capture relevant transactions. In the event of any change (during the year) the Directors are required to make a further declaration to the Company Secretary. Directors refrain from participating at meetings in which lending to related entities are discussed to avoid any kind of influence. Transactions carried out with related parties (RP) as defined by the Sri Lanka Accounting Standard – LKAS 24 on ‘Related Party Disclosures in the normal course of business are disclosed in Note 62 to the Financial Statements. Directors interest in contracts with the Bank which do not fall into the definition of Related Party Transactions (RPT) as per LKAS 24 are reported separately in the Annual Report, outside the Financial Statements. |

✓ | ||||||||||||||||||

| 3 (7) (ii) | RPT covered by direction |

A comprehensive RPT Policy was formulated during the year, which was reviewed and recommended by the BRPTRC and was approved by the Board. This Policy was later circulated among the relevant staff for adherence. The RPT Policy approved by the Board covers the following transactions:

|

✓ | ||||||||||||||||||

| 3 (7) (iii) | Prohibited transactions |

The Banks RPT Policy prohibits transactions which would grant RPs more favourable treatment than that accorded to other customers. These include the following:

|

✓ | ||||||||||||||||||

| 3 (7) (iv) |

Granting accommodation to a Director or a close relation of Director |