Accounting for Capitals - Social and Network Capital

Customers

Commercial Bank is a key partner in the socio-economic progress of each village, town, city or country we operate in and are an integral part of the community. Our business model is based on a deep understanding of the customer needs as we grow together – ‘in step’ with our customers.

Performance Highlights

Figure – 26

Customer Satisfaction

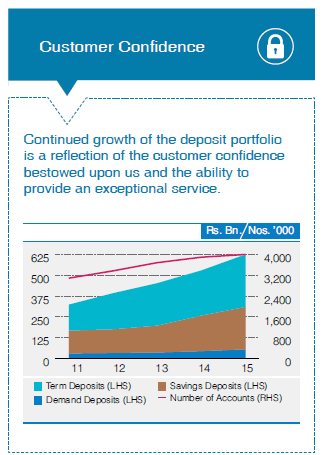

Customers drive our growth and are the front and centre of our business. Growth of our customer base also serves as a barometer of customer confidence and sustainable growth of our business. A growing network of customer touch points, connects us to our customers whilst enhancing accessibility of financial services. Increased hours of operations and investments in state-of-the-art technology, taking banking to the comfort of customers’ offices and homes, enhances customer convenience, driving customer satisfaction.

The past few years demonstrated a set of gratifying results in terms of Customer Satisfaction, with Commercial Bank emerging highest across all key banks in the Truly Loyal customer segment percentage scores. The said scores are evidence that we have exceeded the norms in customer commitment and continuation of relationship building.

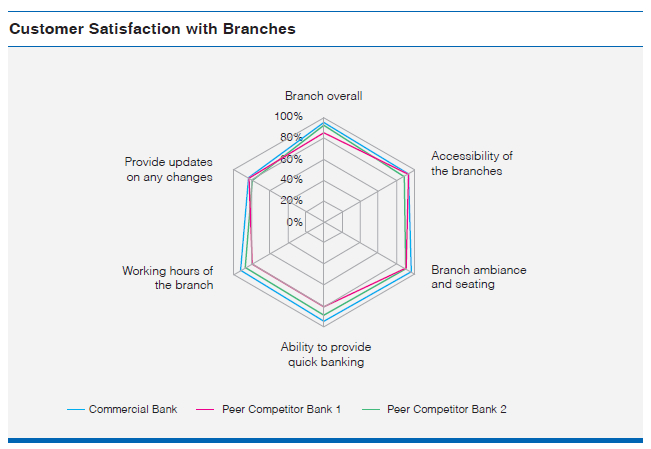

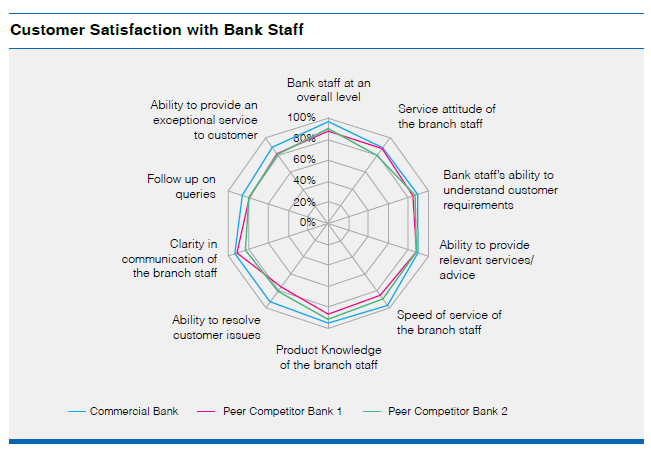

Our bi-annual brand health survey (Figure 26) too has indicated positive results on customer satisfaction amongst current Commercial Bank users, surpassing that of our competitors especially on extended banking hours, branch ambience, and the speed of service at branches. Furthermore, the knowledge of branch staff on products and services along with their ability to provide an exceptional service, follow-up on queries, ability to disseminate relevant information to customers and the ability to understand customer needs have gained a very high score, yet again surpassing that of peer banks.

We continued to enhanced customers’ wealth through a range of innovative products, providing opportunities for investment and disbursing loans that empower their socio-economic progress with advice and guidance on managing transactions, whilst minimising risk.

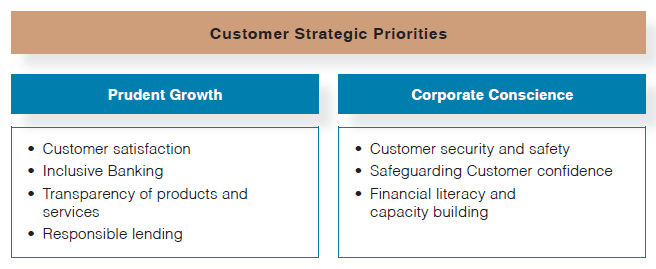

Inclusive Banking

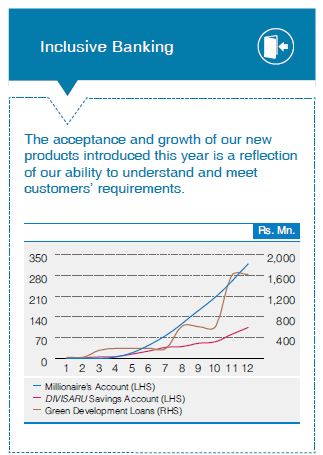

A customer penetration rate of 13%, is testimony to the progress made in financial inclusion, strongly supported by 50% of branches located outside the principal province. The distribution of deposits (Graph 66) and growth of specialised products for women (Anagi Savings Accounts) and senior citizens (Udara Savings/Fixed Deposit Accounts) (Graph 67), also demonstrate our understanding of the requirements of these customer segments and efforts to cater to their needs, including them in the country’s socio-economic progress. Continuing with our efforts to cater to the needs of all our customers the Bank added 12 more branches to the list of branches equipped with wheel chair ramps bringing the total to 130 branches from 118 in 2014, facilitating our differently abled clientele to access customer areas and ATMs. Visually impaired customers also have the ability to enlarge text on our online banking product empowering them to conduct their own banking transactions.

Deposits Distribution – 2015Graph - 66 Growth of Specialised ProductsGraph - 67Accessibility to Financial Services

The Bank has established a presence in the Northern and the Eastern Provinces of the country which were ravaged by a 30-year ethnic conflict which ended in 2009. Our offices in these provinces are staffed with employees who are able to converse in all three official languages (Sinhala, Tamil and English) to ensure that they are able to understand the customers’ requirements and also clearly explain the terms and conditions of our products in the customers’ language of choice. Product information and marketing materials are also developed in all three languages to facilitate access to information in their language of choice. The lowest number of touch points in any province is 2 per 100,000 population and this number moves up to 5 in the Northern Province due to recent initiatives of the Bank to provide access to banking services.

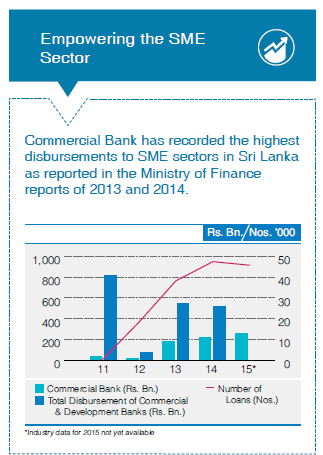

Commercial Bank has recorded the highest disbursements to SME sectors in Sri Lanka, as reported in the Ministry of Finance Reports of 2013 and 2014 (Graph 68). Our widespread branch network and our robust Development Credit Department has been a resounding success in understanding, identifying and developing the needs of the people, offering agricultural and industrial loans at reasonable interest rates, repayment programmes to match the customer’s exclusive cash flow constrains and minimum collateral.

Disbursements to SME SectorsGraph - 68Affordability of financial services is a key aspect of financial inclusion. Our customers have been the beneficiaries of the streamlining of operations, as we reviewed fees and interest rates to ensure affordability of financial services. We participate in 3 loan schemes operated by the CBSL, to enable our customers to gain favourable interest rates from these specialised loan schemes, of which over 2,500 customers received financial assistance amounting to Rs. 1,457 Mn. in 2015.

Transparency of Products and Services

Our Customer Charter ensures that there is transparency in our fees and charges and that customers clearly understand the terms and conditions of the financial products and services used by them. Our friendly and courteous staff explain the products to customers in their language of choice, using flyers that can be retained by customers, which contain information regarding features of the products and their terms and conditions. Deposit rates, lending rates, exchange rates and tariffs and charges are published on our website and updated on a daily basis. Additionally, customers can obtain further clarifications from our Information Centre or any branch. The Complaints and Grievances procedure, is also set out on the website and displayed at branches including contact details of officials of the Bank and the Financial Ombudsman, who can also be applied to in the event efforts made by the Bank, prove unsatisfactory to the client.

Responsible Lending

We are a conservative bank and we encourage our customers to be as conservative in managing their wealth. Consequently, we do not engage in promoting consumption loans, focussing instead on lending products that support wealth creation, such as home loans and business loans. Whether it is for retail or corporate customers, our front line employees are trained to understand customer needs and proffer advice accordingly in keeping with our Code of Conduct and Business Ethics. Screening of business loans to ensure compliance with our Social and Environmental Management Systems (SEMS) Policy, ensures that our customers reap the benefit of our expertise in this regard, whilst we ensure that projects financed by us are in compliance and defined with environmental and social criteria more fully explained on this report

Customer Security and Safety

Customer security and safety is a key priority for the Bank and is regulated by the Banking Act and subsequent Directions, issued by the CBSL in this regard. Measures taken by the Bank in this regard include:

- All employees take an oath of secrecy

- Confining employees’ access to sensitive information through strict controls set in to information systems

- Specific restrictions on disclosure of account information to third parties

- Investments in securing customers online privacy and protection

- Regular compliance reviews

and audits - Certification on specific aspects, benchmarking international best practice

Commercial Bank has been the industry leader in customer protection, in full compliance with the 27001:2013 certification for the past 6 years and we go beyond these requirements, in ensuring the robustness and security of our technology platforms.

Safeguarding of Customer Confidence

The Bank has strict internal controls in place that aim to curtail any form of corruption across the organisation, safeguarding customers’ confidence on the Bank. Our efforts in this regard are implemented by the Inspection Department, which carries out onsite and online surveillances adopting a risk-based approach through which the scope and frequency of audits for each branch or department is established.

The Bank also has an ongoing programme that actively works to prevent money laundering and any activity that facilitates the financing of terrorism and other unlawful criminal activities. Our Anti-Money Laundering Unit, headed by the AML Compliance Officer, centrally monitors transactions and any alerts are promptly reported to the Financial Intelligence Unit of the CBSL.

Financial Literacy and Capacity Building

We support our customers’ growth through capacity building programmes, which build on needs identified through our engagement mechanisms. External bodies that provide specialised skills are identified by the Bank, using our social networks to partner in delivery of these programmes. During the year we conducted 15 such programmes covering 1,822 beneficiaries as depicted in table 29 below:

| Location | Target Group | Programme Focus |

No. of Beneficiaries |

| Ambalantota and Hambantota | Rice millers | Financial literacy and Capacity building | 26 |

| Anuradhapura | Entrepreneurs | Capacity building | 179 |

| Bandarawela | Tea small holders Dairy farmers Vegetable farmers | Financial literacy and Capacity building | 150 |

| Elpitiya | Entrepreneurs | Capacity building | 173 |

| Galenbindunuwewa | Paddy farmers | Financial literacy | 120 |

| Hingurakgoda | Seed paddy farmers | Capacity building | 119 |

| Kandy | Entrepreneurs | Capacity building | 137 |

| Kattankudi | Dairy farmers | Financial literacy and Capacity building | 139 |

| Kuliyapitiya | Entrepreneurs | Capacity building | 124 |

| Kurunegala | Coconut growers | Capacity building | 58 |

| Mullaitivu | Farmers Entrepreneurs | Financial literacy | 130 |

| Nochchiyagama and Thambuttegama | Paddy farmers | Financial literacy | 149 |

| Point Pedro | Small scale fishermen | Financial literacy and Capacity building | 105 |

| Ratnapura | Tea small holders Entrepreneurs | Financial literacy and Capacity building | 145 |

| Silawathurai and Muththarippu | Seaweed cultivators | Financial literacy and Capacity building | 68 |

| Total Beneficiaries | 1,822 |

Table – 29

Business Partners

Over our 95-year history we have developed strong relationships spanning the globe that support and enhance our ability to create value. Our approach is to develop win-win relationships that enable us to grow together, based on a common understanding of values that underpin our transactions. During the year, we have made payments over Rs. 4.0 Bn. to our business partners and engaged in a constructive manner, facilitating their growth. This accounts to over 90% of our total payments to suppliers during 2015.

Figure – 27

Management Approach

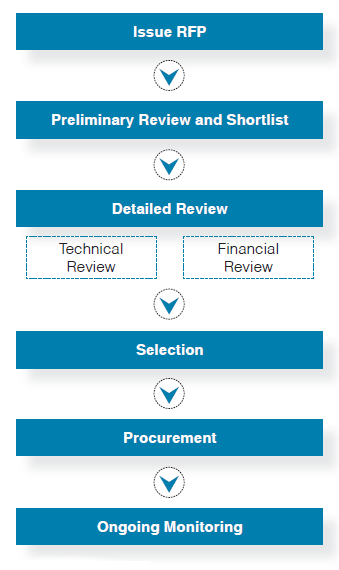

The Bank has an established process to ensure that we engage with business partners in a fair and transparent manner and that our business needs are met without compromise on agreed deliverables (Figure 28). It ensures that a thorough technical review, including social and environment aspects, are reviewed in addition to the financial review and areas of concern are addressed in ongoing dialogues. Commencing with the issue of a Request for Proposal (RFP) on internal approval of the business case, the procurement process ensures ongoing evaluation of our business partners, to maintain standards in-line with our evolving business needs as set in adjacent diagram.

Figure – 28

The RFP issued to potential suppliers include the following requirements:

- Compliance with environmental standards

- Restriction of hazardous substances directive

- Energy star rating

- Adherence to software piracy regulations, as per Intellectual Property Act No. 36 of 2003 and the Computer Crimes Act No. 24 of 2007

- Adherence to the 10th Principle of the United Nations Global Compact (UNGC)

- Adoption of health and safety standards for suppliers with workers at risk of injury or disease

Non adherence to these requirements, results in disqualification from the selection process and may lead to the removal of suppliers from the registered list of suppliers. Regular dialogue ensures that, areas of concern are identified and resolved wherever possible. However, exit clauses in contracts ensure that the Bank is able to terminate the relationships in extreme cases, where material issues remain unresolved.

Our engagement with suppliers maybe routine or ad hoc and also the level of dependency can vary significantly as some categories are critical to our operations. They can be broadly categorised according to these criteria as depicted below:

Figure – 29

Extending Our Reach

A network of 50 correspondent banks, 4 franchise partners, 109 exchange houses and agents facilitate global connectivity across over 200 countries. Our correspondent banks include some of the world’s largest financial institutions and are amongst the oldest relationships with 10 relationships spanning over 25 years. A complete list of our correspondent banks is given on this report. Our Franchise partners include MasterCard, VISA, China UnionPay and Discover which enable us to connect to global payment platforms, facilitating trade and tourism locally and internationally. They are also key partners in product innovation, as we collaborate to introduce appropriate products for the country. Exchange houses and agents facilitate remittances to and from Sri Lankan and Bangladeshi citizens working overseas and are a vital link in this high growth business segment. As with other suppliers, these partners are selected carefully with detailed agreements, defining mutual obligations and performance is monitored by both parties to ensure compliance with agreed terms and conditions.

Critical to Operations

These are suppliers with whom we engage frequently and whose services are required for business continuity. They include electricity, telecommunications, transport and material suppliers including those for standby arrangements with whom we have long relationships. We have identified emissions and health and safety of their workers as the key concerns with these providers and typically engage with transport providers to ensure that they comply with relevant regulatory requirements in this regard.

Ongoing Support

We engage with these suppliers on a frequent basis, as they provide services that are necessary for the smooth functioning of our business covering a wide range of services. They also range from large corporates to SMEs and individuals. Sustainability challenges identified in this segment are depicted in Table 30.

| Business Partner | Areas of Concern |

| Maintenance | Labour Practices Health and Safety of Workers Effluents and Waste |

| Human Resource Providers | Labour Practices Human Rights Health and Safety of Workers |

| Waste Management | Effluents and Waste |

Table – 30

As registered suppliers in this segment are subject to ongoing monitoring with a regular dialogue enabling discussion on areas of concern, we work with suppliers on the identified issues, encouraging adoption of best practice. It should be noted that compliance with all applicable regulations is a requirement across all suppliers.

Ensuring the Well-being of Our Outsourced Staff

The Bank outsources non-critical functions to reputable agencies that meet our rigorous selection criteria. A well-documented screening process, ensures that areas of concern identified by the Bank are subject to high levels of scrutiny. These include compliance with labour laws, ensuring preservation of human rights, minimum pay, timely payments and payment of statutory levies. We also ensure that they get leave, have reasonable working hours and that there is no forced or child labour. The Human Resources Department of the Bank is responsible for the screening of agencies, as they are well versed in the regulatory requirements and are able to guide agencies towards adopting increasingly higher standards in this regard. Additionally, the Security Department of the Bank confirms payment of minimum wage to all security personnel provided by agencies. Half yearly returns for Employees’ Provident Fund and Employees’ Trust Fund are checked by the Human Resource Department for all outsourced staff providers. The Bank’s Internal Audit Department provides assurance on the functioning of processes in this regard.

Non-Routine Engagements

These suppliers range from large scale corporates who provide premises to micro entrepreneurs who provide ancillary services. Suppliers in this category are less rigorously monitored for social and environmental concerns, except for contractors where we work together with them to ensure the health and safety of their workers.